The Beginner’s Guide to Credit Card Travel Hacking

Most people think traveling in business class or staying in luxury hotels is reserved for rich people. We’ve done both many times without paying anywhere near the full price. The secret isn’t how much money you have; it’s understanding how credit card points actually work. Banks have the system put in place, you just need to understand the rules, and we’ve spent more than a decade playing this game so we’ve seen many different credit card travel hacking strategies and evolutions of how things work.

What Are Credit Card Points?

Credit card points are rewards programs that banks and travel companies use to incentivize spending on their products. What makes them so valuable is the economics behind them: airlines and hotel chains make enormous money from these partnerships. Last year it’s estimated that Delta earned more from their credit card partnership ($5B) than they did from flying people around ($3.1B)! Banks earn on annual fees and interest; travel companies earn on brand loyalty. The result is a system where, if you play by the rules, cardholders capture real value.

The rules matter and that’s what we want to help people out with. If you understand the rules, you can capture large amounts of value from credit cards. However, this only works if you pay your balance in full every month. Carrying a balance means interest charges that will take away from the points value that you earn, this is what banks are counting on in order to make money from the deal. Treat your credit card like a debit card by spending only what you’d spend anyway and make sure to pay it off monthly.

What’s the Difference Between Points and Miles?

The terms get used interchangeably, but there’s a useful distinction:

- Miles usually refer to airline-specific currencies (United MileagePlus, Delta SkyMiles). Less flexible, but often more powerful for specific routes.

- Points typically refer to all other reward programs, including hotel loyalty programs (Marriott Bonvoy, World of Hyatt, Hilton Honors) and transferable rewards (Chase Ultimate Rewards, Amex Membership Rewards). In the case of transferable rewards, their value comes from flexibility. You can move transferable rewards to multiple airlines or hotels.

How to Figure Out Where to Start

Before opening any card, start with the trip. Pick somewhere that you actually want to go, whether that be a safari, Everest Base Camp, a beach week in Southeast Asia or whatever else your heart desires and work backwards from the most expensive part. Doing this helps remove some of the uncertainty of where to start, because once you narrow what sort of experience you’re trying to have, then you can use that to inform which credit card you should sign up for.

For most international trips originating in the US, flights are the big-ticket item. For domestic or shorter trips, hotels might be where the real savings are. Once you know which kind of trip you’re targeting, you can choose cards that earn those specific currencies. Another secondary consideration is your travel style, some people will get more value from a few nights in 5 star resorts, while others would prefer longer stays in more budget friendly destinations.

When we planned the first leg of our trip around the world, going from the United States to South Africa, flights were going to be the expensive piece and we knew we wanted to go business class, because the total travel time is 30+ hours and that’s if you’re lucky enough to find a flight with a short layover.

In order to research which kind of miles to use, you generally would have to spend many different hours on other points blogs researching programs (One of my favorites is DoctorOfCredit) but since it’s 2026 and we have the technology now, a simple prompt to your favorite AI chatbot (we use a mix of Claude and Gemini) would work:

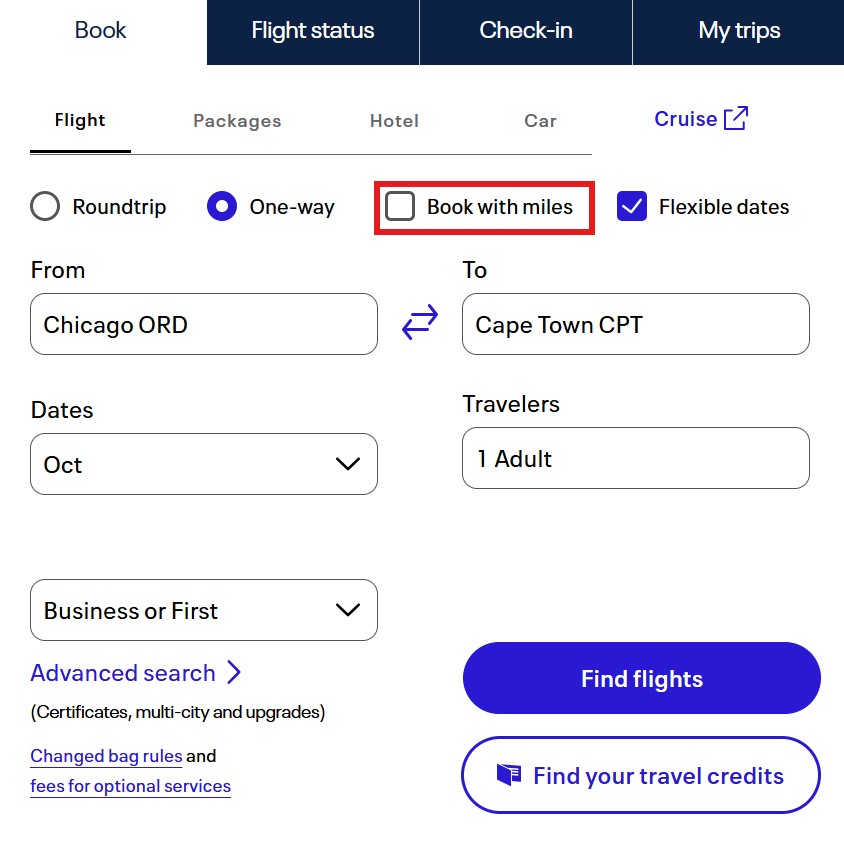

This will give you a list of the types of points and miles to start researching. After we had the list of programs, we started searching for flights on the different program’s flight award search tools! Each frequent flier program will have an option to change the payment method to award miles and then you can see how much award flights cost, when they are available, and what routes are possible.

Award availability varies but generally you have to search 3-6 months out, and the further out, the more likely you have options. Same thing with hotel availability, the further out you search, the more options that will be available.

After researching award availability, the best value we found was using United miles on Ethiopian Airlines in business class. United miles were recommended from our search above, and you can use the United search tool to find partner flight bookings in addition to United’s own flights. For long international trips, partner bookings are usually better value and cost less miles. The cost was 88,000 miles + $42 in taxes per person. Had we bought those seats with cash, they would have cost more than $3,500 each!

To get those miles, we each opened a United card and hit the minimum spend requirement ($3,000 in purchases within the first 90 days). Once we did, the 80,000 mile sign-up bonus deposited into our frequent flier accounts and we had enough miles to buy the flights while only having to pay the $42 in taxes!

How Do Credit Card Sign-Up Bonuses Work?

Sign-up bonuses are the engine of credit card travel hacking. Card issuers want new customers, so they offer large point bonuses (typically 50,000 to 100,000 points) to incentivize sign-ups. Earning the bonus requires that you need to spend a minimum amount (usually $3,000–$5,000) within the first 60–90 days of opening the card. Hit that threshold and the points deposit automatically.

In our case, one sign-up bonus covered a business class flight that would have cost $3,500 in cash. That’s the math that makes this worth paying attention to.

A few things worth knowing: the minimum spend is designed to be reachable through normal daily spending, as a beginner you should focus on cards where you can hit the bonuses without having to make extra purchases outside of your normal spending. The annual fee on most travel cards ($95–$550) is almost always offset by the sign-up bonus alone in year one.

The Best Starter Card for Most Travelers

If you’re new to points and want one card to begin with, we recommend the Chase Sapphire Preferred ($95 annual fee). Here’s why:

- Earns transferable Chase Ultimate Rewards points (transferable to United, Hyatt, Southwest, and more)

- 2x points on dining and travel

- No foreign transaction fees, which matters when you travel internationally

- Points are redeemable for cash back

The sign-up bonus from this card varies over time, but it is generally worth about $500–$750 in travel when transferred to partners!

We’re covering credit card strategies in more depth as we go! Check out our credit card strategy for couples post for how we stack sign-up bonuses together, sequence which card to get next, and stay within issuer rules like Chase’s 5/24 and Citi’s 48-month rule. We’re still planning to dig into transfer partner sweet spots in a future post. Sign up for our email list below to be notified when new posts drop!

If you have any questions about any specific cards or want to learn more about credit card travel hacking, reach out to us on social media @CheckedOutToCheckIn and we’ll be happy to answer them!

This post contains affiliate links for the things we love. If you sign up for the card at the link above, we may earn a small commission at no extra cost to you. This helps us keep the blog running! 🙂

One Comment